Where now for European banks? Sir Howard Davies, former chairman of Britain's Financial Services Authority, said on BBC Radio's Today programme on Tuesday morning that he thought the French government was only days away from having to recapitalise the country's banking system for a second time. It's hard to disagree.

The panic seems to have been temporarily stemmed by a statement from BNP Paribas to the effect that it wasn't having the problems widely reported of finding dollar funding. There was also an emphatic denial of discussions over state intervention. But no-one is kidding themselves. Italy had to pay the highest spread since joining the euro to sell its bonds on Tuesday. There are growing fears over whether Europe's largest borrower can stay the course.

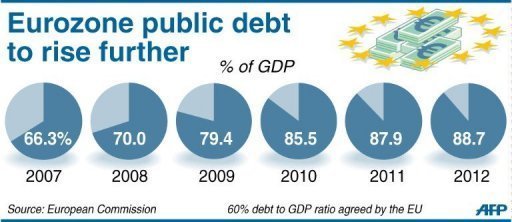

The eurozone sovereign debt crisis is meanwhile exacting a devastating toll on the European banking system as a whole, the UK included. With their high exposure to eurozone debt, the problem is particularly acute for the French banking goliaths, BNP Paribas and Societe Generale.

BNP alone has a eurozone sovereign debt exposure of some €75bn, amounting to roughly 6pc of total assets, including €14bn of Greek debt and €21bn of Italian government bonds. And that's just BNP. The other two major French banks, SocGen and Credit Agricole each have exposures of a similar order of magnitude. Collectively, French banks have €56bn of Greek sovereign bonds alone. They've so far only written down this Greek debt by around 20pc, or in line with the restructuring agreed at the time of the last bailout.

That's nowhere near mark to market. In the increasingly likely event of Germany kicking the Greeks out of the eurozone altogether, Greek debt will become close to worthless. Greece is already effectively a cash only economy. Most forms of credit has effectively dried up, the Greek banking system is finished, and capital controls to prevent what little money that remains from leaving the country are surely only a matter of time. European banking must prepare for the worst as far as Greece is concerned.

As for the remainder of the eurozone sovereign exposure, there's been no write down at all among banks on these bonds. If there's a wider problem of default, the bad debt recognition has yet to come.

How come European banks have got so much of the stuff? Well ironically, this is one lending decision gone wrong that the banks cannot be blamed for. In response to the original banking crisis, regulators ordered banks substantially to increase their liquidity buffers. Government bonds are generally viewed as the most liquid and least risky assets to hold, so that's where the money went.

That these regulatory obligations also helped governments fund their ever growing deficits is by the by. In any case, nowhere is the law of unintended consequences more in evidence than in financial regulation. By seeking to address the last crisis with greater liquidity buffers, regulators succeeded only in sowing the seeds for the next one. A banking crisis that transmogrified into a sovereign debt crisis now shows every sign of transmogrifying back into another banking crisis.

Much of the selling pressure on European banks has come from the US. American investors and lenders look at Europe and see a Continent apparently incapable of gripping its problems. With the debt crisis approaching some kind of self evident denouement, there's no-one in charge, only denial and blame. Policymakers seem more concerned with the irrelevancies of moral hazard than on finding solutions. If it wasn't so tragic, it would be laughable. Europe is fiddling while Rome burns.

When the banking crisis first broke, Europeans tended to regard it as wholly an Anglo-Saxon problem. There was some recapitalisation of French and German banks that went on in late 2008, early 2009, but it wasn't nearly as big as in the UK and the US, and within a year, the French banks had in any case largely repaid all their state support. Problem over, it was thought.

The same refusal to face up to underlying solvency concerns continues to dominate Contintental attitudes to the crisis. There is a collective sense of denial. BNP for one insists that it is in nothing like the same poor shape as many UK and US banks back in 2008. Profits are still buoyant, delinquency subdued, and capital more than adequate, BNP insists. Unfortunately, that's not what the markets are saying.

Record quantities of European term funding are set to mature in the first quarter of next year. It's not clear that the European Central Bank can cope with the sort of liquidity support that banks will require if markets refuse to refinance it. Europe's financial and monetary system is falling apart.

Since French banks are widely thought of as essentially arms of the French state, is there actually any point in recapitalising them? In France, the public subsidy issue which has so exercised the Vickers Commission on banking in the UK is taken for granted. Banks are understood to be underwritten by the state, and therefore require less capital and can hand the benefits of cheaper funding onto to their customers. Why not then just make this implicit support explicit?

You only need to take one look at what happened to Ireland to see why. In the early days of the crisis, the Irish government promised to stand behind all banking liabilities. By doing so, it ended up pushing the entire country into bankruptcy. No. France and Germany need to recapitalise their banks. The sooner they do so, the sooner the wider programme of debt forgiveness necessary to set the European economy back on a sustainable footing can begin....

Geithner: Economy in "an early stage" of crisis.

International alarm over euro zone crisis grows.

Moody's cuts French banks, eurobond talk lifts markets.

Markets in thrall to eurozone worries

Greek PM to hold crisis talks with Merkel, Sarkozy.

Banks already dealing with the Greek inevitability.

Greece gets closer to the brink: Merkel and Sarkozy to hold talks over debt crisis

.... It certainly does not look good, this assessment.

stating the obvious.

No comments:

Post a Comment